Disrupting the Banks

How did a startup from Melbourne become one of Australia's biggest banks?

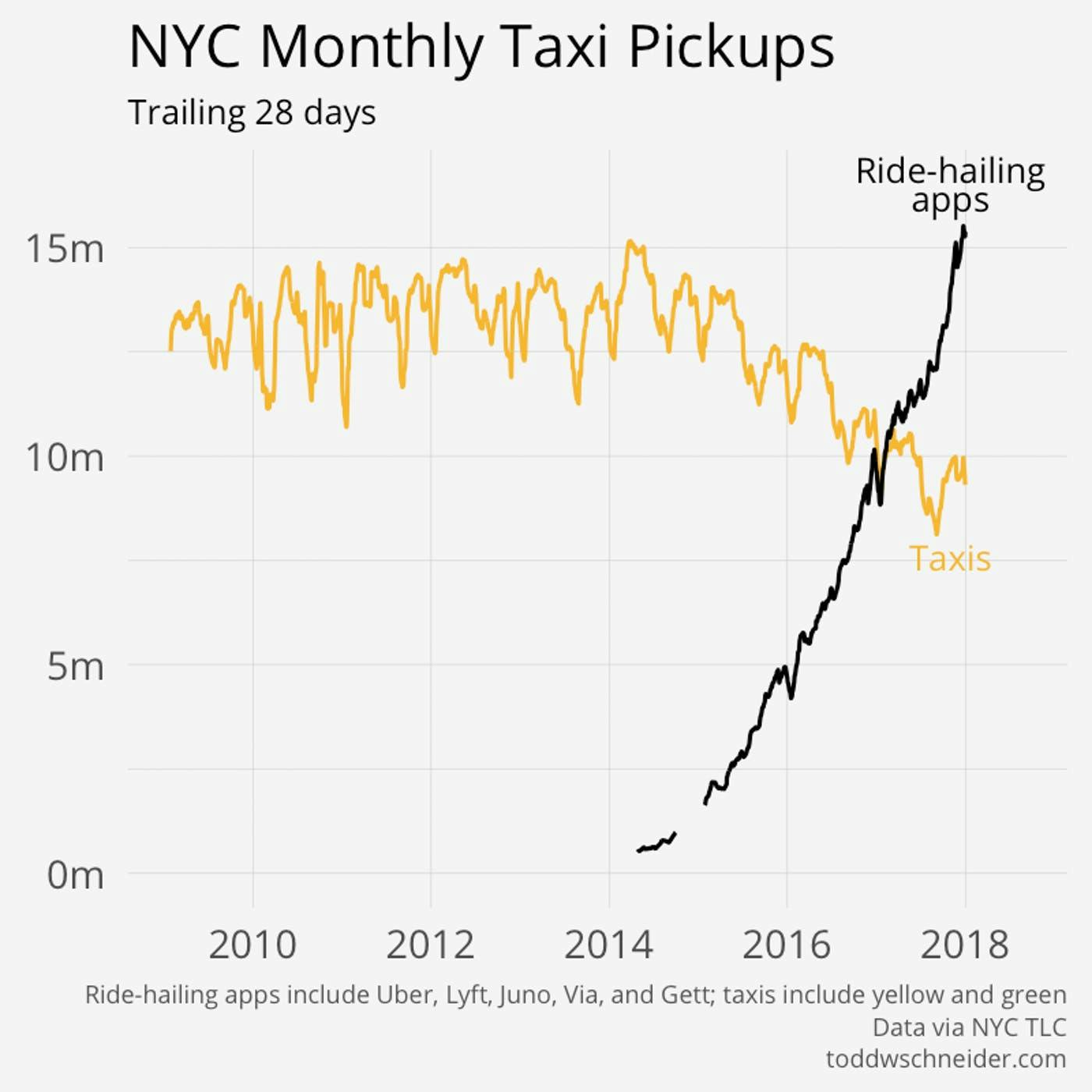

There's a chart I've been facinated with ever since I was shown it. It presents the disruption that Uber created in the driving industry when it first entered the New York City market. Having near exponential growth for the first few years Uber quickly overtook the taxi industry in New York City. It's a stark reminder to stagnant industries that disruption can come when you least expect it.

§Banks Used to Suck

Additionally the lack of competition made the products provided by banks almost identical. A savings account with almost no interest, a transaction account with a monthly fee, credit cards that have huge fees and interest rates. This only grew resentment, but most customers didn't have any better alternative - as can be seen on the below chart until 2013 refinancing stayed quite low.

At around the same time a number of smaller "neobanks" started to begin operating in Australia, these banks were met with mixed success but lot of fan-fare as disgruntled customers were keen for a better deal.

Around the year 2015 the bulk of millennials started to reach the age where they had significant savings and full time employment. With that this mobile first generation started to look for a better way to manage their money.

Some readers might not know what a "neobank" is, if you're familiar with the traditional system of banking you'd expect a bank to have physical branches where you can go to deposit and withdraw your money. A neobank is different, for starters they have no physical branches and operate entirely online, because of this the types of services they provide are also quite different to a regular bank. Generally only providing basic transaction and savings accounts.

But neobanks have offered another product to consumers - Trust.

This is also a deeper problem than what a PR blitz can fix, the underlying issues go beyond branding as any reasonably good marketing company can help a company look good.

§The Rise of Neobanks

Up is a great case study about the success a business can have when it focuses on customer outcomes and not what the industry it's based in is doing.

§A Better Culture

In Australia the "big 4" major banks have roughly 73% of the Australian banking market, that's down from 79% in 2013^[4]. It's not enough for companies to do what their competitors are doing and simply catch up, doing so will only stop the loss of customers and will not be able to bring old users back.

Up differentiated themselves early on as not being your parents bank. They didn't have a home loan product, and they still don't offer credit cards. They sold the idea of a responsible bank that would help you save money and support initiatives that would help the environment.

I asked some Up customers what they like about the culture and platform compared to their old banks and got a mix of different opinions. Matthew Timms put it together quite nicely;

The Australian banking landscape, prior to the wave of neobanks, was an impersonal hellscape. Banks served businesses & home loaners; there was no rush to make the individual banking experience any better.

Up, as a startup, needed to focus on user growth & they did so through developing an intuitive & enjoyable user experience which felt like a breath of fresh air. They scooped up millennials who felt neglected by big banks - they didn't own businesses nor mortgages. But they will in a decade.

So as the wave of neobanks comes to an end, as we see many of them close their doors, Up stands by far the most successful Aus neobank & a fascinating story of industry disruption. Pfhfhf I could start a podcast about it but it wouldn't be very interesting.

The story of Up's success if not a new one. There will be other companies that disrupt industries and innovate ultimately delivering better outcomes for consumers. The reason Up is so interesting is because it's a case study of how customer loyalty can be earned when a company embraces their customers.

§Getting in my DMs

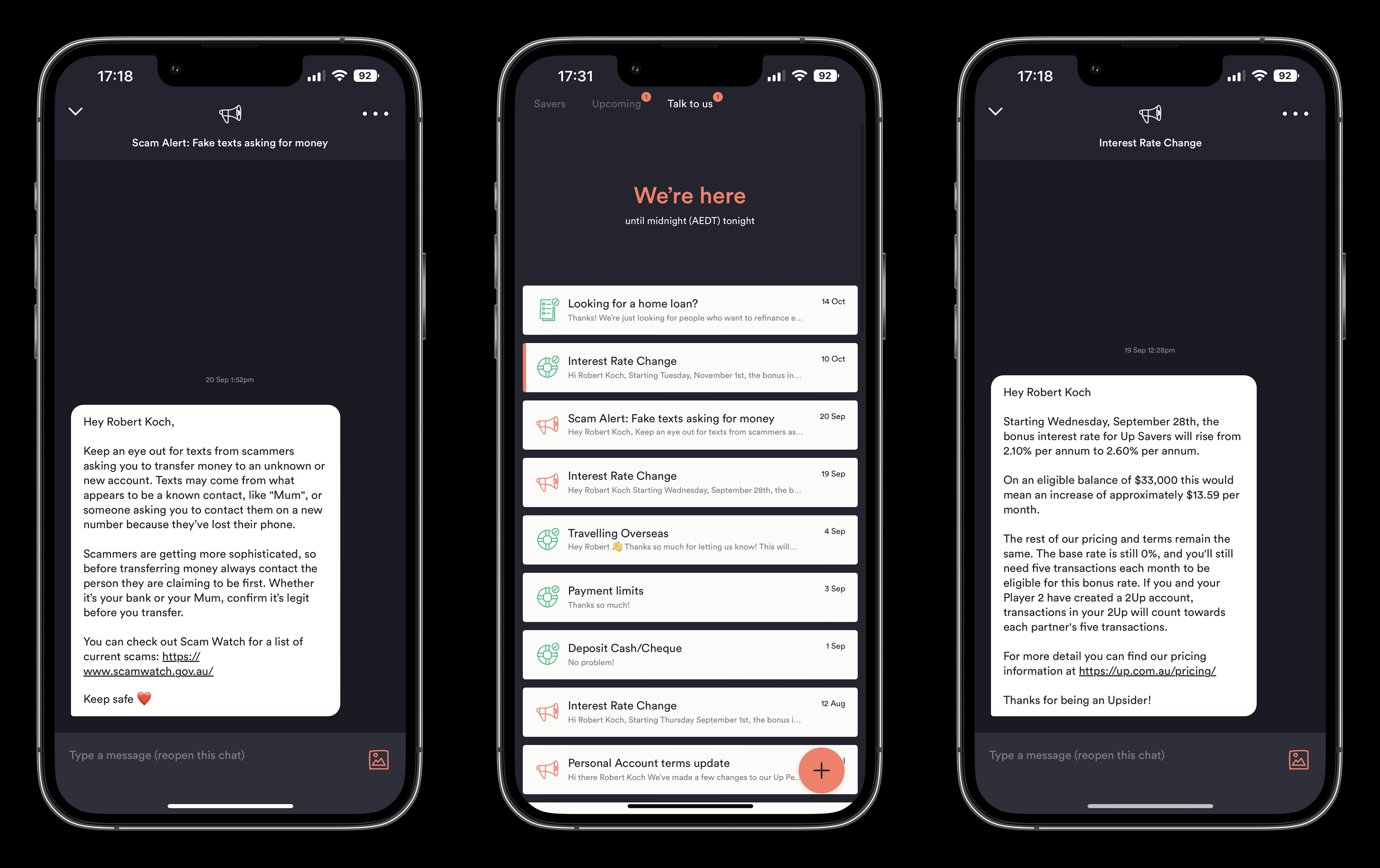

This is done via their in-app communication panel which allows customer support staff to talk to customers live without the need for a branch. Where traditional banks require a customer to travel to a branch or pick up the phone to get support all Up customers do is start a DM. Additionally the process is asynchronous - so you can do other things while you're waiting for a response. This is how disruption benefits consumers, while Up wasn't the first company to add live chat in-app it was certainly the first bank in Australia to do so and now most of them has some form of similar feature.

As you can see from the screenshots below the asynchronicity of getting support is a big part of the experience, allowing customers to go through their day instead of lining up at a branch.

Earning trust with consumers is an incredibly hard endeavour, a piece of advice one of my managers gave me not to long ago when dealing with this is to "over-communicate" - that's exactly what Up does with its customers and is what I see as the second reason that it's done such a good job at disrupting the hold the "big 4" banks have on Australia.

§Features

Hugo was the person that introduced me to Up way back in 2017. He's a software engineer and I asked what he was excited about when he first heard about Up.

The added bonus of releasing new features means that people are more engaged with the brand. Wanting to have the latest and greatest is a powerful incentive to convince consumers to use your product. I asked a few people about what features they care about in a banking app and a point that Emma Scully made sums up nicely how Up has managed to attract a large group of followers.

Up has re-framed my online banking into more of a organisational and productivity oriented experience rather than just an app where one can view their balance and transfer money. You don't typically hang out for a new update or follow the Instagram page of your usual banking apps, but Up brings exciting new features that actually gets you following your bank's social media to keep up.

§Final Thoughts

Don't stop innovating. Like in the case of Uber - when an industry stops innovating it will eventually be disrupted. A new business model or company that can shake up the market will do it. If Ups success indicates anything it's that if the banking industry can be disrupted, any industry can be.

§Footnotes

-

So the statistic I read this for I forgot to write down but this article by Fast Company talks about a similar trend of millennials preferring to work at a sustainable company over a higher paying job. ↩

-

This is actually something that Amazon prides itself on as well, by not looking at what competitors have done and listening to customers some of AWS most successful services like RedShift and Aurora have been released. ↩